A SSAS is a flexible pension scheme with many advantages over more conventional schemes.

One of the advantages of a SSAS is the ability to purchase a wide range of investments and products. This includes purchasing commercial property, making loans to companies or third parties, and the ability to purchase other types of non-standard investments, such as unquoted shares.

What is an unquoted share?

An unquoted (or unlisted) share is a share of a private company which is not listed on a recognised stock exchange, for example the London Stock Exchange. Traditionally they are shares in small to medium sized companies and can be considered as “higher risk” than more conventional investments, however they can be a valuable asset for the right investor.

Can my SSAS invest in unquoted shares?

The short answer to this is yes, your SSAS can invest in unquoted shares.

As with any investment you need to be sure you understand all the risks involved and, if necessary, seek independent financial advice.

For any client considering this type of investment we would expect them to have previous experience in investing in unquoted shares, be a high net worth individual or perhaps be seen as a sophisticated investor. There are also some limitations which are governed by HMRC.

What are the HMRC limitations on unquoted shares?

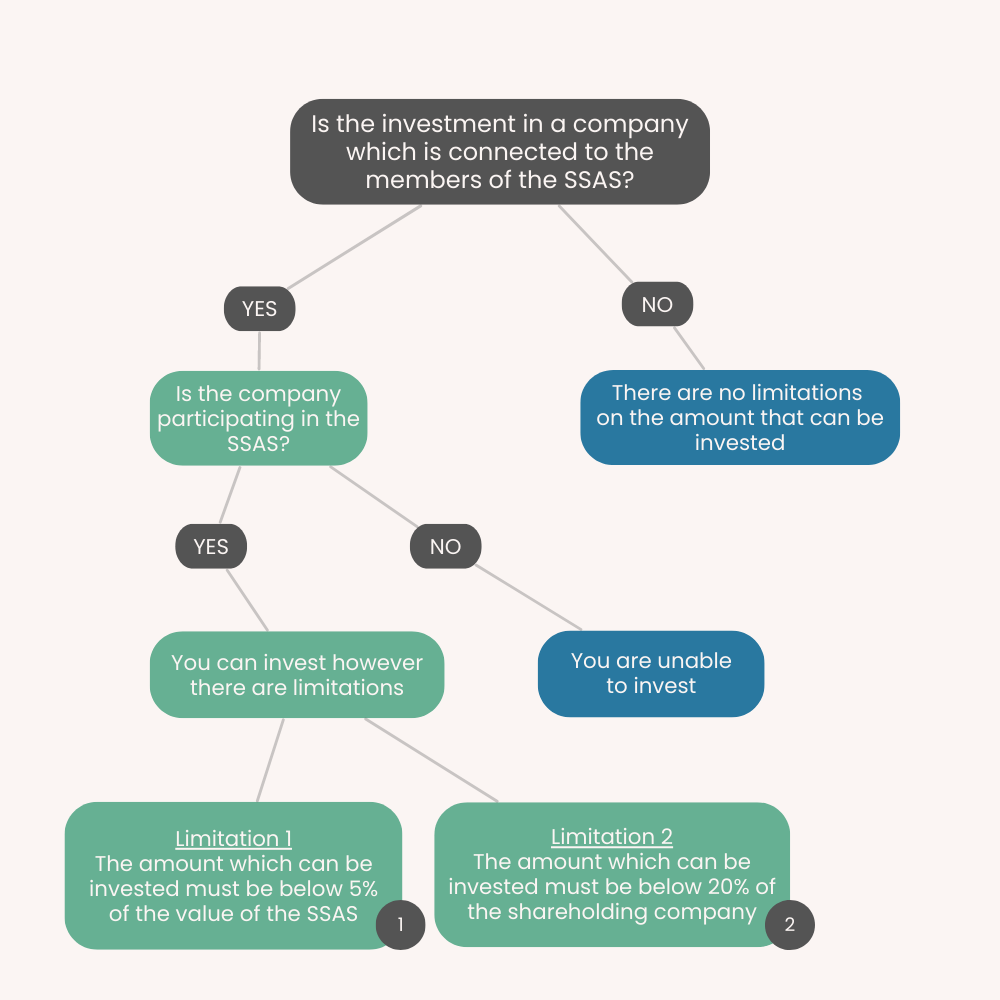

This largely depends upon:

- whether the investment is in a company which is connected to the members of the SSAS, and

- whether the company is participating in the SSAS.

I’ve broken this down in the diagram below:

1. This is the net market value of the assets of the SSAS as at the date of purchase. This means any liabilities (for example a mortgage) will need to be taken into account and investment valuations may need to be brought up to date.

2. If the company in which you are looking to invest in owns more than £6,000 of taxable property (for example computer equipment, furniture, and machinery), the amount that can be invested is limited to less than 20% of the company’s shareholding (10% if it’s an investment company). This limit applies to all the scheme members and any connected parties. i.e. the combined total shareholding between the SSAS, the scheme members and any other connected parties, in respect of an trading company needs to be below 20%.